Vaccination rollouts en masse

Global shares fell 0.8% and 0.4% in hedged and unhedged terms, respectively. Global equities were influenced in part by volatility in US markets. Sizeable retail-initiated positioning in certain small stocks triggered de-leveraging (selling positions) by investors and contributed to broader market weakness. In addition, concerns additional stimulus would not be forthcoming weighed on the US market.

- Emerging markets rose 3.7% during January outperforming developed markets. This was due to a strong bounce back by Alibaba following the reappearance of co-founder Jack Ma and removal of US delisting fears following President Biden’s inauguration.

- Australian shares outperformed global shares rising 0.3% in January. The market was led by strength from the financial (up 2.2%) and energy (up 1.3%) sectors. Energy stocks rose in line with continued strength in oil prices as investors anticipated economic recovery (and higher oil demand) after vaccination rollout.

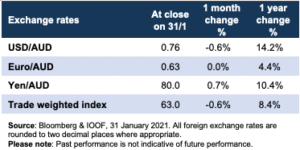

- The Australian dollar (AUD) fell 0.6% against both major currencies and the US dollar.

- Fixed income returns were negative following rising bond yields domestically and internationally. Stronger economic results with Europe for example seeing a better-than-expected decline in Q4 economic activity stoked conviction in the recovery theme.

As coronavirus cases slow

Globally

- Coronavirus case growth globally appears to be materially slowing. Vaccine rollouts appear to be having an impact with the rollout in Israel performing well in protecting more vulnerable elderly victims according to the Israeli Ministry of Health.

- We saw an orderly transition to the new Biden Administration in the US with the signing of new Executive Orders flagging a commitment to climate change policy while President Biden also signalled plans for further fiscal stimulus.

Locally

- The RBA left interest rates on hold at 0.1% while announcing a further $100bn in bond purchases at its February meeting. This is designed to keep borrowing costs low for both governments and businesses while also maintaining downward pressure on the Australian Dollar.

- The unemployment rate fell to 6.6% in December, pleasingly declining from 6.8% in November thanks to continued strong jobs growth.

- Geopolitical tensions with China remained but did not accelerate in January.

Major asset class performance

Currency markets

| Indices used: Australian Shares: S&P/ASX 200 Accumulation Index, Global shares (hedged): MSCI World ex Australia Net Total Return (in AUD), Global shares (unhedged): MSCI World ex Australia Hedged AUD Net Total Return Index; Global small companies (unhedged): MSCI World Small Cap Net Total Return USD Index (in AUD); Global emerging markets (unhedged): MSCI Emerging Markets EM Net Total Return AUD Index; Global listed property (hedged): FTSE EPRA/NAREIT Developed Index Hedged in AUD Net Total Return; Cash: Bloomberg AusBond Bank Bill Index; Australian fixed income: Bloomberg AusBond Composite 0+ Yr Index; International fixed income: Bloomberg Barclays Global Aggregate Total Return Index Value Hedged AUD

Please note: Past performance is not indicative of future performance |